Buy your home with me!

Use a real estate pro

Owning your own home is one of the most rewarding experiences you’ll ever enjoy. But how much you know about the buying process—and whom you choose to help you—can save you from unnecessary headaches and unforeseen hassles. This is where I come in—offering the guidance, information and assistance that only a qualified real estate professional can provide.

There are many aspects of the home buying process that require explanation and the more you know, the better position you will be in when it’s time to sign papers, many of these things may have changed.

And because I stay on top of all the latest real estate laws and regulations, you can rest assured that you are always getting the expert advice and service you deserve. Helping my clients achieve their real estate goals is my top priority. I’d welcome the opportunity to be your trusted partner.

I can also help you team up with some proven financial experts to put the best loan package together—for you. When you have a dedicated team working together on a planned strategy, chances are you’ll be moving into your dream home sooner than you might imagine.

If you’re ready to discuss how we can work together to take your home search to the next level, please don’t hesitate to call. I live in Lake Ridge, Woodbridge VA 22192 but I also have offices in Alexandria, Tysons Corner, Vienna, and Chantilly. Call/text now 703.659.7763 or email me at [email protected]

The Buying Process explained

First of all, congrats on this big decision – buying a home is a very big deal! It’s one of the largest financial decisions you are going to make. This decision will also determine your lifestyle, your monthly budget and your long-term neighbors. My point is – don’t take it lightly.

Due to the size of this responsibility I have a process to help my clients buy a perfect home. I don’t just put you in my car and start showing you houses – most of the time that’s a waste of your time and mine. If you just want to pick houses off the internet and see them – use Redfin, Zillow, Trulia. If you want to get clear about what you need, want and consider all your options, then here is how I can help.

1. THE VERY FIRST STEP is for us to chat over the phone or email. I want to find out the basics – why are you looking to buy, when and what areas you are considering. I will also ask you about your price range and if you had a chance to talk to a lender (if not – not to worry). Once we chat we will set up a time to get together and discuss your home buying much deeper.

2. CONSULTATION. Usually we get together at my office at 4500 Pond Way in Lake Ridge, ste.100 Woodbridge, VA. Here is what we discuss:

- Your current situation

- What is your search criteria for the new home

- How I can help you achieve your goals

- Buying process: loan, making an offer, contract period, closing costs

- Current market conditions

- Paperwork for me to represent you (if that’s what we want and decide)

- Look through available listings in MLS with your search criteria and select the ones you’d like to see. I use an elimination process vs. selection – so we will consider all homes within your search criteria and then eliminate the ones that won’t work. This way we will make sure we are not missing out on anything.

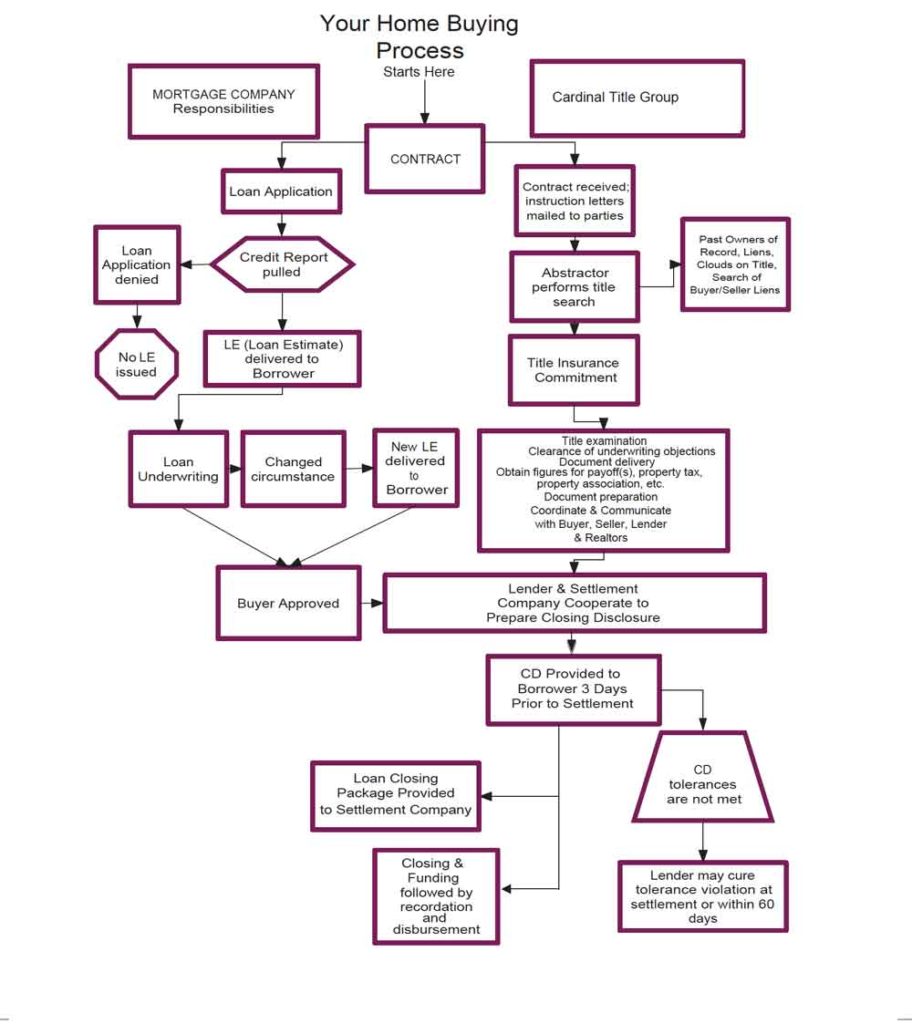

3. LOAN PRE-APPROVAL. Before we start looking at homes – you will need to get a loan pre-approval from a lender. With all the media talking about strict lending guidelines – there are lots of options for buyers with low down payments. Once you have a pre-approval letter – we can start looking at homes. I will be glad to work with your lender or I can recommend you a couple of awesome guys!

4. HOME VIEWINGS. This is the fun part – at least in the beginning. Some homes are vacant, but many are occupied and need an advance notice for showings. During our 1st tours we will see ALL listings that might work for you. Our goal will be to keep a roll of top 3. There is no 100% perfect home – if it’s 90% perfect – it’s probably the right home for you. If we find “the home” that you are interested in – we will make an offer. If not – we will continue looking. I will set you up on automatic listing updates from our MLS that has the most accurate and up-to-date listing information. We will be keeping track of the market together and the minute the right home comes along – we will jump on it quickly. Keep in mind the best listings usually sell in a few days.

5. OFFER SUBMISSION. Once we find the perfect house we will make an offer. We will look up similar homes that sold in the area to make sure we don’t offer too much. There are standard forms that we use for all resale transactions in Norther Virginia to make an offer. There are similar forms for DC and MD, but they are different jurisdictions with slightly different form requirements. Most important items that seller will be looking for:

- Offer price

- Closing cost credit from the seller towards your closing costs

- Earnest Money Deposit (good faith deposit – I usually explain this in person)

- Settlement date

- Type of financing and lender’s reputability

- Items that we expect the seller to leave in the house (we will mark all appliances that stay, etc)

- Inspections: home inspection, termite, radon, possibly lead based paint

- Other contingencies – financing, appraisal

- Potential pre-settlement or post-settlement occupancy

If the house has been on the market for a while – there usually is a lot more negotiating with the seller. In this case we go back and forth a few times and play an increment game. If the house just hit the market and we are competing with an 2nd offer – we will have no negotiating power and will try put put our best foot forward right away – no playing games.

6. CONTRACT PERIOD. Let’s say the negotiations went well and we have a ratified contract (that’s what the final agreement is called). This process is usually 30-60 days. During this process we will be doing our due diligence and will be removing the contingencies one by one. Your chosen lender will get the loan process started and order an official property appraisal. Title company will be making sure you will be receiving a clear title. We will be scheduling inspections, moving money for the down-payment, fulfilling every lender’s request and reviewing condo/HOA docs. Buyers have a few ways to cancel the contract: home inspection, HOA condo/document review. If the appraisal comes in lower than the sales price and the seller does not agree to lower it – you have the right to cancel the deal.

7. WALKTHROUGH INSPECTION. Right before the final signing we will get a chance to go to the property and inspect if the home is in the same condition and if all agreed upon repairs were completed.

8. SETTLEMENT (OR CLOSING). The final signing is called a settlement. Usually is happens at the physical location of the Title Company. You will have to bring your ID’s and the remainder of the down payment. Once all the documents are signed and the money is delivered to the Title agent – you get the keys! Yay! You can move in! Congratulations!!!

There are a lot more details in this process and I did not want to overwhelm you! I usually walk my clients through all of them in a timely manner. During the contract process I send my clients a email every week with a to do list – so they know what to expect.

If you have any questions about the process – please don’t hesitate to ask. I’m here to help!

The VA Residential TERMS explained

REAL PROPERTY: The first paragraph of the Contract details, with specificity, the Property that is being conveyed.

PRICE AND SPECIFIED FINANCING: The financing terms for the transaction, as well as the sales price, are outlined in this paragraph. The Purchaser is able to indicate the down payment, and the amount(s) of financing in dollar amounts or percentages of the sales price. There are provisions for the purchaser to obtain a first deed of trust, a second deed of trust, or to assume the seller’s loan(s). The type of loan, term of years and interest rate also are included in this section.

DEPOSIT: This paragraph details the earnest money deposit that the Purchaser provides to the Escrow Agent in the form of a check or promissory note. The Selling Broker is typically chosen as the Escrow Agent; however, the Settlement Agent or another party may be selected. The Purchaser also must select whether the earnest money deposit has been delivered to the Escrow Agent at or prior to contract ratification, or whether it will be delivered a defined number of days following ratification.

SETTLEMENT: The Settlement paragraph sets forth the settlement date and the settlement agent. It also gives notice to the Purchasers of their right to choose the settlement agent in accordance with the Real Estate Settlement Agents Act (“RESAA”).

DOWN PAYMENT: The balance of all money due from the Purchaser must be paid at closing by certified funds or bank wired funds (no personal checks). If the Purchaser is to use an assignment of funds at settlement (typically from the sale of another property immediately prior to their purchase settlement), the Seller’s written consent must be obtained.

DELIVERY: This paragraph specifies the general delivery requirements under the Contract (except for delivery of documents pursuant to the Virginia Property Owners’ Association Act and the Virginia Condominium Act). The parties select the allowable method(s) of delivery and fill in the blanks with the corresponding physical address, email address and/or fax number. (Contrary to prior versions of the contract, there is no longer a mandate that courtesy copies be sent to the Brokers.)

VIRGINIA RESIDENTIAL PROPERTY DISCLOSURE ACT: The Seller must deliver a disclosure statement prior to acceptance of the Contract (unless the property is exempt). If the disclosure is delivered to the Purchaser after the Date of Ratification, the Purchaser will have a limited right to terminate the contract subject to the provisions of the Act.

VIRGINIA PROPERTY OWNERS’ ASSOCIATION ACT: The Seller must obtain an Association Disclosure Packet from the association and provide it to the Purchaser. The Purchaser provides in the contract a preferred address for delivery of the Disclosure Packet by both electronic means and hard copy. The seller may then choose the address to which to deliver the Disclosure Packet. This section also provides for the Purchaser’s right to cancel the Contract following receipt (or prior to receipt) of the Disclosure Packet, subject to the time periods defined in the Act.

VIRGINIA CONDOMINIUM ACT: The Seller must obtain a Resale Certificate from the association and provide it to the Purchaser. The Purchaser provides in the contract a preferred address for delivery of the Resale Certificate by both electronic means and hard copy. The seller may then choose the address to which to deliver the Resale Certificate. This section also provides for the Purchaser’s right to cancel the Contract following receipt of the Resale Certificate, subject to the time periods defined in the Act.

PROPERTY MAINTENANCE AND CONDITION: The Seller must deliver the Property in “substantially the same physical condition” as on the date specified in the contract, and “broom clean with all trash and debris removed.” This paragraph also notes that except as otherwise specified in the Contract, “the property, including electrical, plumbing, existing appliances, heating, air conditioning, equipment and fixtures shall convey in its AS-IS condition as of the date specified.” Some suggestions for addressing this provision include the following:

a) The condition of the Property must be verified on the date specified in this paragraph.

b) The walk-through inspection is intended to be a quick check of major systems/appliances; it is not a new “home inspection.”

c) Don’t wait until the very last minute to conduct the walk-through inspection as this may delay your Settlement and does not leave enough time to repair items that may need to be fixed prior to Settlement.

d) Be sure the Seller leaves utilities on through Settlement.

There are also checkboxes to indicate whether the Contract is contingent on a Home Inspection.

ACCESS TO PROPERTY: The Seller must provide reasonable access to the Purchaser, Broker, inspectors, Lender representatives, etc. in order to comply with the Contract. Walk-through inspection(s) may be done within 7 days prior to settlement and/or occupancy.

UTILITIES WATER, SEWAGE, HEATING AND CENTRAL AIR CONDITIONING: There are several checkboxes to describe the water system, sewage, disposal system, heating and air conditioning for the Property. If the Seller discloses that a Septic Waiver has been granted on the property, the Purchaser should review the regulatory requirements and cost associated with repairing the sewage system. State Board of Health Septic System Waivers are not transferable.

PERSONAL PROPERTY AND FIXTURES: This section contains an itemized list of various personal property and fixtures that will convey with the Property. Check EACH item “Yes” or “No” and if more than one is to convey, fill in the number of each item that will convey.

FIRPTA – WITHHOLDING TAXES FOR FOREIGN SELLERS: This section requires the Seller to disclose whether they are a US Citizen or a Lawful Permanent Resident. If not, an additional addendum is required in the contract.

FINANCING APPLICATION: The deadline for the Purchaser to make a written loan application for the Specified Financing defined in paragraph 2 AND for any lender-required homeowner’s insurance is 7 days after the date of Contract Ratification. The Purchaser also gives the Selling Company and the lender permission to disclose general information about the loan application progress and approval process to the Listing Company and to the Seller.

ALTERNATIVE FINANCING: The Purchaser may substitute alternative financing and/or an alternative lender for Specified Financing provided that:

a. The Purchaser is qualified for alternative financing;

b. There is no additional expense to the Seller; and

c. The Settlement Date is not delayed.

The parties must refer back to paragraph 2 (Price and Specified Financing) for the specific financing terms. As long as the Purchaser’s financing terms do not deviate from the terms in paragraph 2, the Purchaser will preserve the protection of the financing contingency. If the financing terms change (i.e., the purchaser switches from a

conventional to a VA loan, or the amount of the down payment and loan amount change), the Purchaser should realize that the financing contingency will not provide a protection if the Purchaser is rejected for the alternate financing, unless the parties execute an addendum amending the Specified Financing.

BUYER’S REPRESENTATIONS: The correct box should be checked as to whether or not the Purchaser will occupy the Property as a principal residence.

SMOKE DETECTORS: The Seller must deliver the Property with smoke detectors installed and functioning pursuant to applicable regulations.

TARGET LEAD-BASED PAINT HOUSING: The Seller shall disclose whether any part of the house or condominium was built prior to January 1, 1978. If so, a Lead-Based Paint Disclosure shall be required, and shall be attached to the Contract.

WOOD-DESTROYING INSECT INSPECTION: The Seller shall be responsible for treatment of any wood-destroying insect infestation, and any repairs noted on the inspection report shall be made at the seller’s expense. All reports must be dated within 30 days of Settlement.

DAMAGE OR LOSS: The Seller is responsible for the risk of loss or damage to the property until delivery of the deed to the Purchaser at Settlement.

TITLE: If the title report and survey are not available on the Settlement Date, the Settlement may be delayed up to 10 business days to obtain the information; thereafter, the Seller has the option to terminate the Contract. If title is not good, marketable and insurable on the Settlement Date, the Purchaser has the option to declare the Contract void or may pursue all available remedies at law. In the alternative, the parties may mutually agree to extend the Settlement Date. If action is required to perfect the title, such action must be taken promptly by the Seller at the Seller’s expense.

NOTICE OF POSSIBLE FILING OF MECHANICS’ LIENS: This section alerts the Purchaser that a mechanics’ lien may be filed after settlement for work performed prior to settlement.

POSSESSION DATE: Unless otherwise agreed to in writing, the Purchaser gets possession of the property at Settlement and the Seller must deliver any keys, key fobs, codes and digital keys.

PERFORMANCE: This paragraph details the sufficient tender of performance under the Contract. Compliance with the Contract can help to preserve a non-breaching party’s right to damages. At a minimum, the Purchaser must have:

• A bank-issued check (payable to Cardinal Title Group) and/or wired funds DELIVERED on or before the Settlement Date to the Settlement Agent;

• A hazard insurance policy in place and a paid receipt for the insurance DELIVERED to the lender at or before settlement;

• A loan package and lender funding at Settlement.

DEFAULT: Even if the Financing Contingency has not been removed, the Purchaser may be in default if Settlement does not occur on the Settlement Date for any reason other than a default by the Seller. In the event the Purchaser is in default, the Purchaser’s deposit may be at risk. Further, the Purchaser should realize that the earnest money deposit may not be the limit of the Purchaser’s liability upon default.

OTHER DISCLOSURES: The Seller and Purchaser are advised to read the Contract and to verify that the terms marked accurately reflect their intentions. In addition, the parties are advised that the Brokers can provide advice on real estate matters, but that tax and legal advice should be sought from the appropriate professionals.